2020 has been a difficult year for nearly everyone in the world, and a devastating year for many. Our smarter and better angels are always looking for silver linings during a crisis. Capital Hall Partners sees a few in real estate.

We know many readers are pretty exhausted by the political cycle and the uncertainties surrounding the pandemic. Hopefully we can offer you a diversion, looking at a few areas of economic strength with constructive longer-term outlooks. In an effort to stay in our lane, we’ll focus on positive trends in real estate that we think readers should know about.

Economists have been increasingly referring to the U.S. economic recovery as “K-shaped.” Some areas of the economy—air travel, brick-and-mortar retail, small businesses, restaurants, hospitality, etc.—are stuck in down cycles and struggling to fully recover.

On the other side of the “K” are businesses thriving in the current environment—enterprise cloud, big tech, consumer staples, e-commerce, and a few key areas in real estate. We’ve been investing in one of the key areas: life sciences.

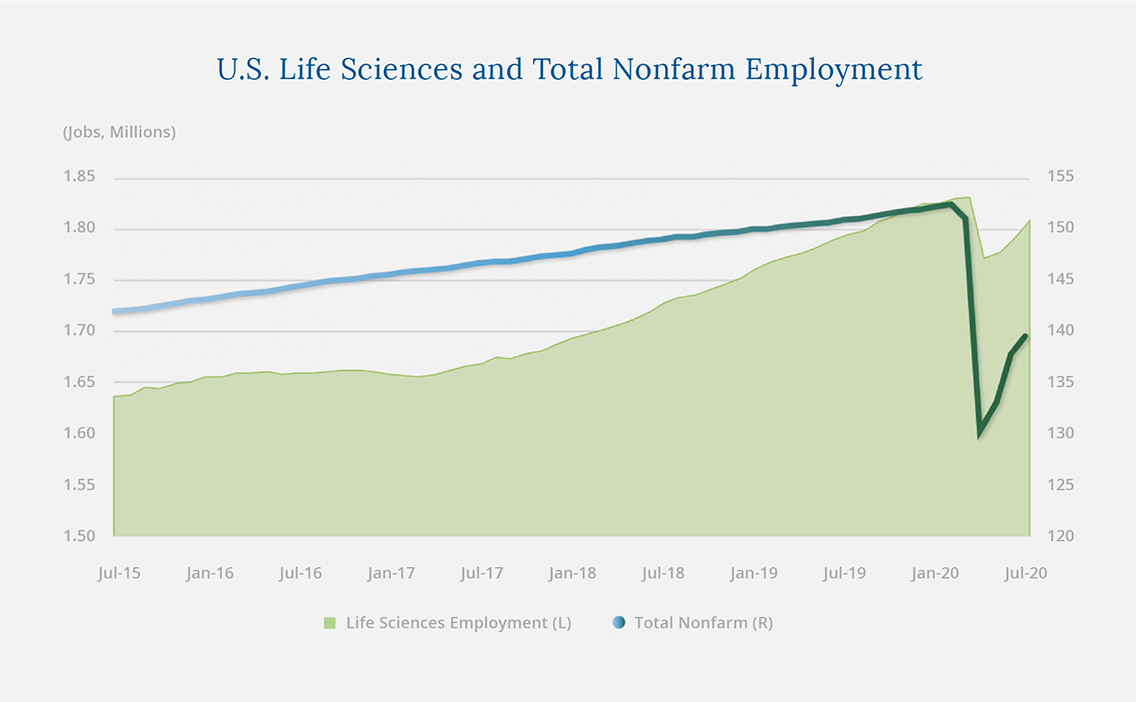

The life sciences industry has moved to the center of the global narrative in 2020, as companies race to develop effective treatments and vaccines. The industry has not been unscathed by the recession, but employment in life sciences has held up remarkably well relative to the broad economy. Biotech research and development employment has been particularly strong, up by 4.9% from a year ago and outpacing tech employment growth.

Life sciences is driving urban-core demand for office and lab space, boding well for commercial real estate investors in the sector.

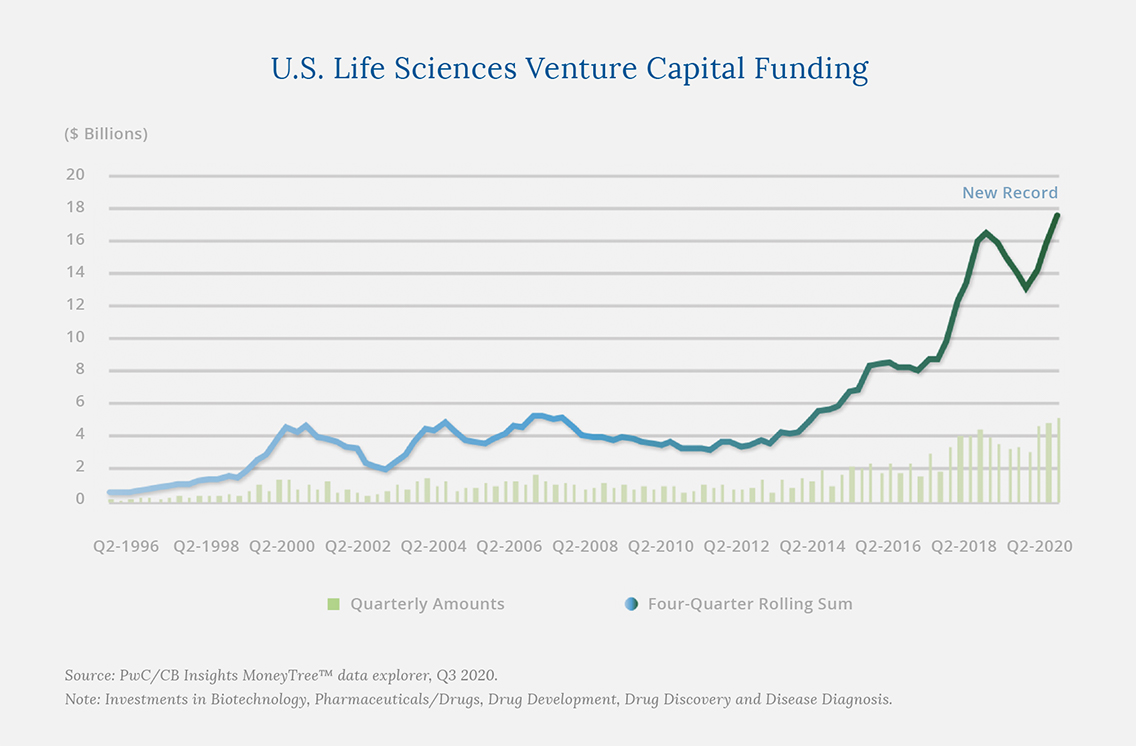

Venture capitalists are also taking note. In response to the pandemic, and because of better understanding of the longer-term threat of pandemics, the U.S. life sciences industry saw its largest quarterly total of venture capital investment in Q2 2020.

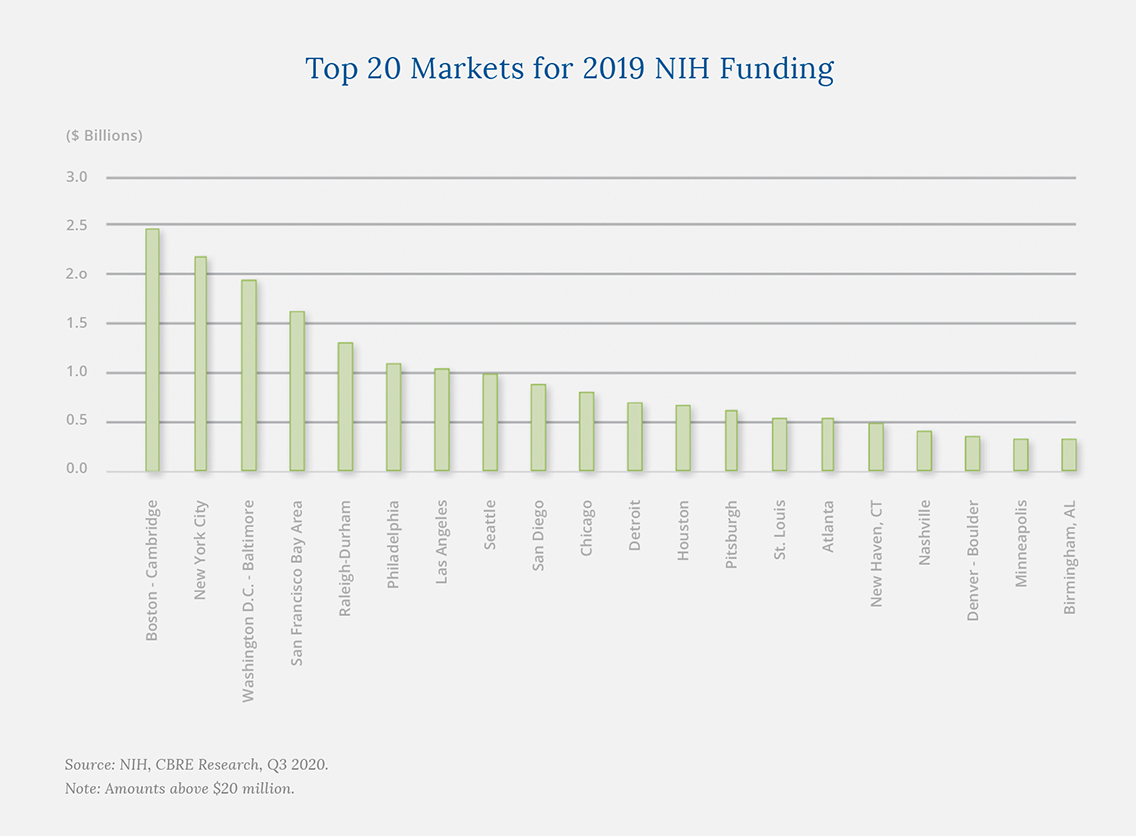

The rolling annual total of life sciences venture capital investment hit a record $17.8 billion in Q2 2020. This surge in funding runs counter to U.S. venture capital investments in all other industries, which have been declining since mid-2019. Another major driver behind the surge in life sciences demand has been the billions of dollars funneled to major universities and research institutions for health-care research from the National Institutes of Health (NIH).

There’s a major silver lining here for commercial real estate investors in life sciences: venture capital and other funding growth has historically preceded employment gains by about year, signaling strong job gains for the industry in 2021.

This correlation between funding and employment provides a direct tailwind for Capital Hall Partners, since 54% of all venture capital investment has been to Boston-Cambridge and the San Francisco Bay Area. We’re developing two Life Sciences campuses in the Greater Boston Area, the Gateway Innovation Center and Brickyard @ Assembly project.

The Boston-Cambridge laboratory market remains tight, with a vacancy rate of just 4.9% in Q2 2020. In the Cambridge submarket alone, a 2.6% vacancy rate helped push average asking rents up by 12.4% since early 2019. As of Q2, nearly 110 tenants were seeking a total of 3.7 million square feet of lab space, up slightly from the beginning of 2020. Compared with a year ago, the number of tenants seeking space has grown by 83%, while total space required is down marginally.

More than 50 companies in the Boston-Cambridge market can apply their science and technology to COVID-related products, which has also created a marginal boost to demand. In the Greater Boston area, we expect more rent growth and extremely tight vacancy in the coming quarters and perhaps years.

We’re grateful to be positioned in what we see as a strong, valuable market with a focus on helping everyone live better, healthier lives.

Another outperforming area of real estate has been housing, which has an indirect effect on Capital Hall Partners’ current projects.

In a sense, housing has been the economic story of the third quarter. The sector declined in-line with the broader U.S. economy in the spring, but has since climbed back to pre-pandemic levels in terms of housing starts and construction.

Downstream effects of the housing boom have been evident in consumer spending on furniture, appliances, and home improvement, which has outperformed spending across most other sectors. Construction employment has recovered briskly. One familiar name in the space, Home Depot, underscores the sector’s strength: the company posted its best quarterly sales growth in nearly 20 years.

Interestingly, much of the new growth is being driven by millennials, who previously had been reluctant to enter the housing market as family formation lagged and as they favored renting. For the first time, millennials accounted for over 50% of new home loans.

Migration out of densely-populated cities is driving a significant portion of this housing strength, which we believe indirectly benefits our QOZ project in Tempe, Arizona—the HUB.

While the HUB in Tempe is an office building, it’s one story and outside of a dense urban area. In fact, it’s the type of market people are leaving dense cities like San Francisco and New York to pursue. The HUB is focused on positioning the property as an environmentally sustainable, Covid-19 safe and healthy building. The HUB will have many distinct competitive advantages to midrise or high-rise office buildings, due to the need to transfer employees to their workspace via elevators—the problem point for physical distancing and the lack of safe and healthy improvements such as air filtration, fresh air intake, touchless entry, lighting and plumbing.

We see tenants gravitating to single story and low-rise office buildings, and in response we are accelerating the buildout of certain tenant improvements such as painting the interior, adding restrooms, and placing the HVAC units complete with high air filtration—all typically done once a tenant has executed a lease. We have made a decision to make the space as “Move-in Ready” as possible, thus shortening the timeline that a tenant can locate in the space, begin paying rent and provide its workers a safe and healthy work environment.

Looking Ahead to 2021

Capital Hall Partners is taking a cautious and patient approach to what we see as a bifurcated real estate market: life sciences, logistics-oriented buildings, data centers, and industrial commercial real estate are holding up nicely. Meanwhile, we fully expect pricing adjustments to the downside in hotel, retail, high density (urban) multi-family, and dense urban office space.

For now, our goal is to focus on the core: the LA, Boston, and Phoenix markets with an emphasis on life sciences, “healthy office,” and industrial commercial real estate. And as ever, we will look for distressed situations where Capital Hall Partners can recapitalize and reposition existing buildings.

For readers and investors who want to learn more about our projects in Qualified Opportunity Zones, the terms of investment, or who have questions about how Qualified Opportunity Zones work, please reach out to us at info@caphall.com. We’d be happy to talk with you.

Capital Hall Partners is a privately-held real estate investment and development firm. We have over 50 years of experience over multiple real estate cycles, with a current focus on value-oriented investments in Qualified Opportunity Zones in the Los Angeles, Phoenix, & Boston areas. Our commitment to investors is to preserve capital, deliver attractive risk-adjusted returns, be trustworthy and transparent.

If you would like to learn more about Capital Hall Partners, Qualified Opportunity Zones, or our work in Boston, please contact us today at info@caphall.com.