Investors can also receive non-taxable cash distributions from any refinancing during the hold period.

Source: Fundrise

Source: Fundrise

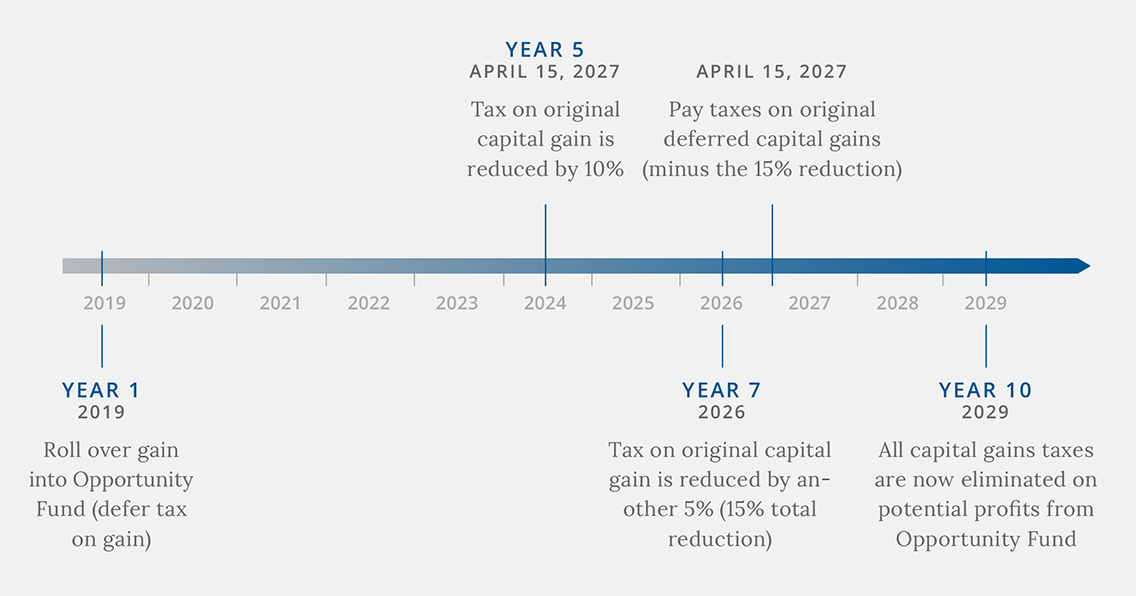

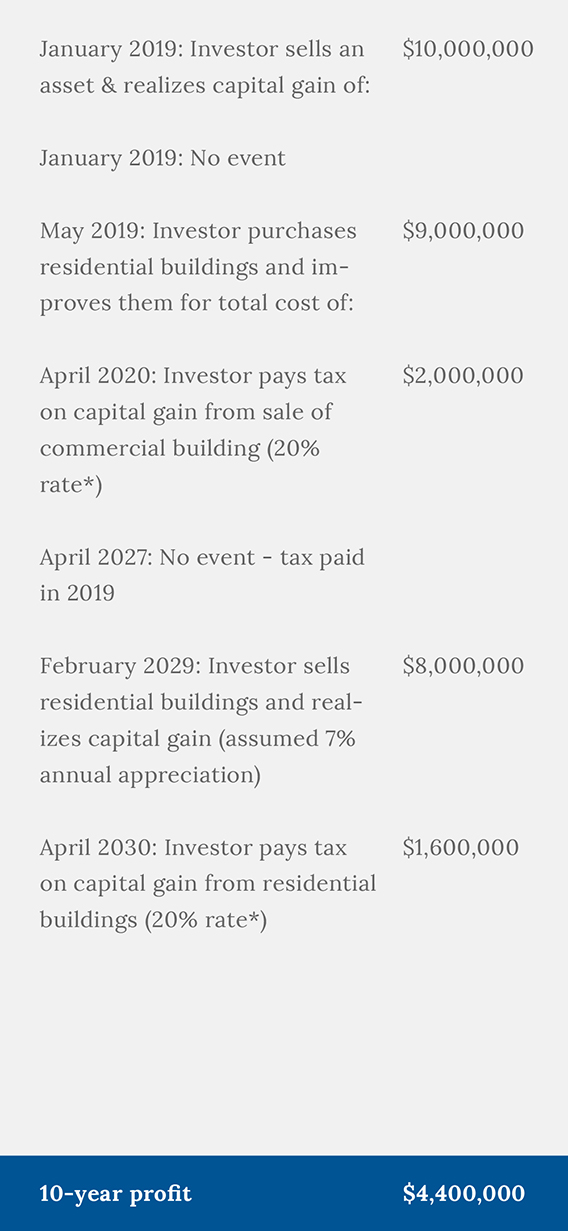

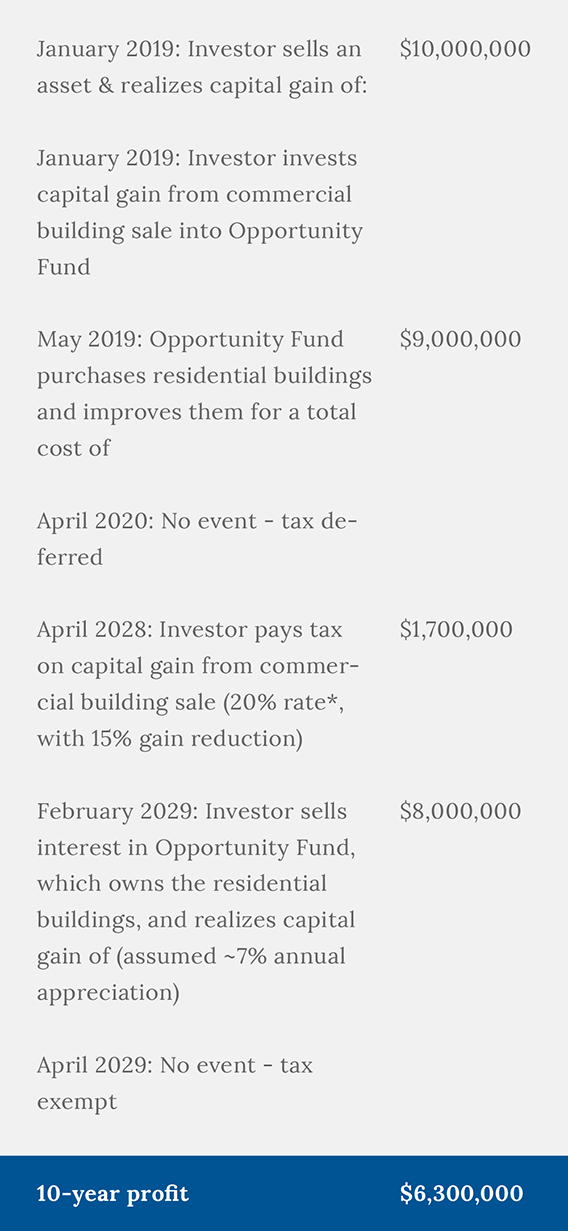

In the hypothetical example below, which uses a 20% capital gain tax rate for the purpose of simplification, a capital gain of $10 million is invested in a traditional real estate investment (left column) vs. an opportunity zone investment (right column). The tax deferrals preserve profit in the OZ program, which generates $6,300,000 over 10 years versus the $4,400,000 profit from the non-OZ real estate deal. QOFs give investors the possibility of achieving attractive, risk-adjusted economic returns enhanced by up to 40% relative to traditional real estate investments.

Traditional Real Estate Investment

Real Estate Opportunities Zones Investment

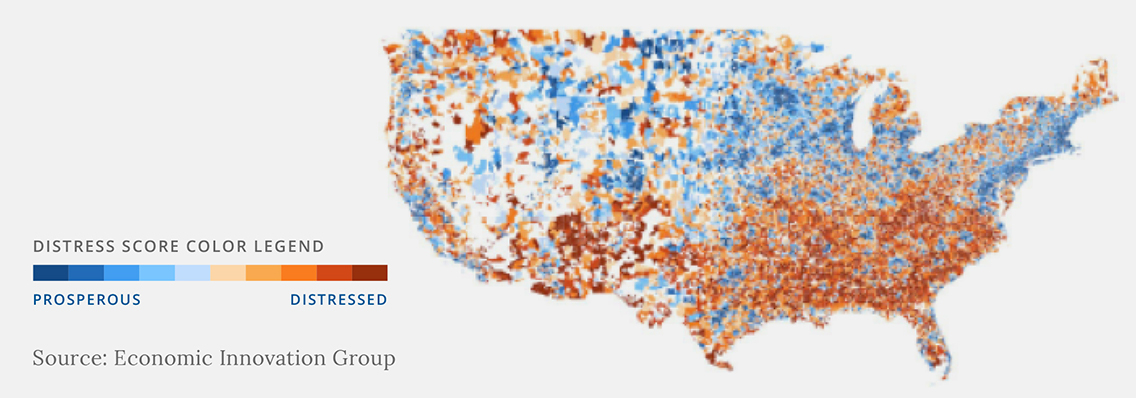

Finally, QOFs promote socially responsible investing and give investors the chance to make a real impact on communities in need of an economic boost. Capital scarcity is a significant issue in certain areas, both urban and rural. The Economic Innovation Group’s research, which inspired the creation of opportunity zones, found “that 50 million Americans live in economically distressed communities,” which contain “1.4 million fewer jobs in 2016 than they did in 2007” – a clear indication of the gap separating areas of need and communities that were able to recover in the aftermath of the Great Recession.

The result is a nation increasingly reliant on certain geographic areas to create new businesses and jobs while other areas continue to languish. QOFs not only have the potential to create this vital infrastructure in opportunity zones—they can also add auxiliary benefits like improved education, developing additional affordable workforce housing, advancing health care access, expanding nutritional options, and improving the prospects for people in more than 8,700 communities across the United States.

Next Step: How to Approach Opportunity Zones

While opportunity zones offer tremendous promise, they present additional layers of complexity relative to traditional real estate investments. The OZ program demands close attention to detail, as well as thorough familiarity with tax law. Capital Hall Partners believes these complexities necessitate a conservative, thoughtful approach to reduce risk and enhance returns – an approach born from years of experience managing complex development projects.

QOF investments are limited to certain types of property: they must be made in either new construction or major renovations or reuse—and renovations must show substantial improvement within 30 months of construction. Substantial improvement requires a QOF invest an amount equal to the building’s basis of the property plus $1 USD, not including land value. We strictly adhere to a disciplined underwriting process to preserve capital, deliver returns, and maintain compliance with these provisions.

Capital Hall Partners focuses QOF investment dollars on properties with great potential regardless of their potential tax benefit. This means prioritizing capital preservation and investing in properties that achieve attractive risk-adjusted returns prior to tax-benefit enhancements: multi-family units, industrial “last-mile” e-commerce distribution, and creative and adaptive reuse projects including industrial conversion.

Our QOF investments greatly reduce or eliminate the use of leverage prior to stabilization of the property, allowing for maximum tax benefit capital as quickly as possible. By placing low levels of leverage during development and higher levels once properties stabilize, we can maximize the QOF tax benefits to investors.

The Bottom Line:

Opportunity zones represent a major opportunity for positive social impact through sustainable, long-term investment – a chance for the private sector to contribute capital to low-income neighborhoods and/or communities already demonstrating growth. Combined with attractive tax benefits, QOFs offer tremendous benefits for investors when managed with an experienced, thoughtful, and prudent approach—which is precisely what we strive to provide at Capital Hall Partners.